Do you have a will, a trust, and retirement accounts? Who will get your retirement assets?

Let’s say that your will says that everything goes to your spouse, your trust says that everything goes to your children, and the beneficiary form for your IRA says that everything goes to your spouse and your children equally. Who gets your IRA? It will go to your spouse and your children equally.

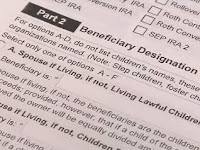

IRAs pass to beneficiaries through the beneficiary form. They don't pass by way of your will unless you name your estate as your beneficiary or sometimes, in what should never be the case, if you fail to name any beneficiaries at all. They also never get to your trust unless you name your trust as your beneficiary. You could have the best trust in the world in place to receive distributions from your IRA after your death, but if you don’t file a beneficiary form naming that trust as your beneficiary, it will never see any IRA distributions.

IRAs pass to beneficiaries through the beneficiary form. They don't pass by way of your will unless you name your estate as your beneficiary or sometimes, in what should never be the case, if you fail to name any beneficiaries at all. They also never get to your trust unless you name your trust as your beneficiary. You could have the best trust in the world in place to receive distributions from your IRA after your death, but if you don’t file a beneficiary form naming that trust as your beneficiary, it will never see any IRA distributions.

Whenever there are changes in your family situation, you need to think about whether your beneficiary forms need to be updated. This is especially true after a divorce or a remarriage. If you do not want retirement benefits going to an ex-spouse, then you probably have to update your beneficiary forms. If retirement benefits are meant to go to children and not to a newly married spouse, then you may need to have the new spouse sign a waiver of his or her rights to your retirement benefits. Without a waiver, the benefits might go automatically to your new spouse, cutting out your children. This is almost always true for employer plan benefits.

When there is no beneficiary form on file, you are really taking your chances. Now your retirement assets will go to whoever the company has named for you in the default language in the documents for the account. It could be a spouse; it could be your estate.

Do your loved ones a favor and make sure your retirement assets are going to the right person - the one you planned on receiving the benefits. Check those beneficiary forms.

-By Beverly DeVeny and Jared Trexler

Let’s say that your will says that everything goes to your spouse, your trust says that everything goes to your children, and the beneficiary form for your IRA says that everything goes to your spouse and your children equally. Who gets your IRA? It will go to your spouse and your children equally.

IRAs pass to beneficiaries through the beneficiary form. They don't pass by way of your will unless you name your estate as your beneficiary or sometimes, in what should never be the case, if you fail to name any beneficiaries at all. They also never get to your trust unless you name your trust as your beneficiary. You could have the best trust in the world in place to receive distributions from your IRA after your death, but if you don’t file a beneficiary form naming that trust as your beneficiary, it will never see any IRA distributions.Whenever there are changes in your family situation, you need to think about whether your beneficiary forms need to be updated. This is especially true after a divorce or a remarriage. If you do not want retirement benefits going to an ex-spouse, then you probably have to update your beneficiary forms. If retirement benefits are meant to go to children and not to a newly married spouse, then you may need to have the new spouse sign a waiver of his or her rights to your retirement benefits. Without a waiver, the benefits might go automatically to your new spouse, cutting out your children. This is almost always true for employer plan benefits.

When there is no beneficiary form on file, you are really taking your chances. Now your retirement assets will go to whoever the company has named for you in the default language in the documents for the account. It could be a spouse; it could be your estate.

Do your loved ones a favor and make sure your retirement assets are going to the right person - the one you planned on receiving the benefits. Check those beneficiary forms.

-By Beverly DeVeny and Jared Trexler

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}